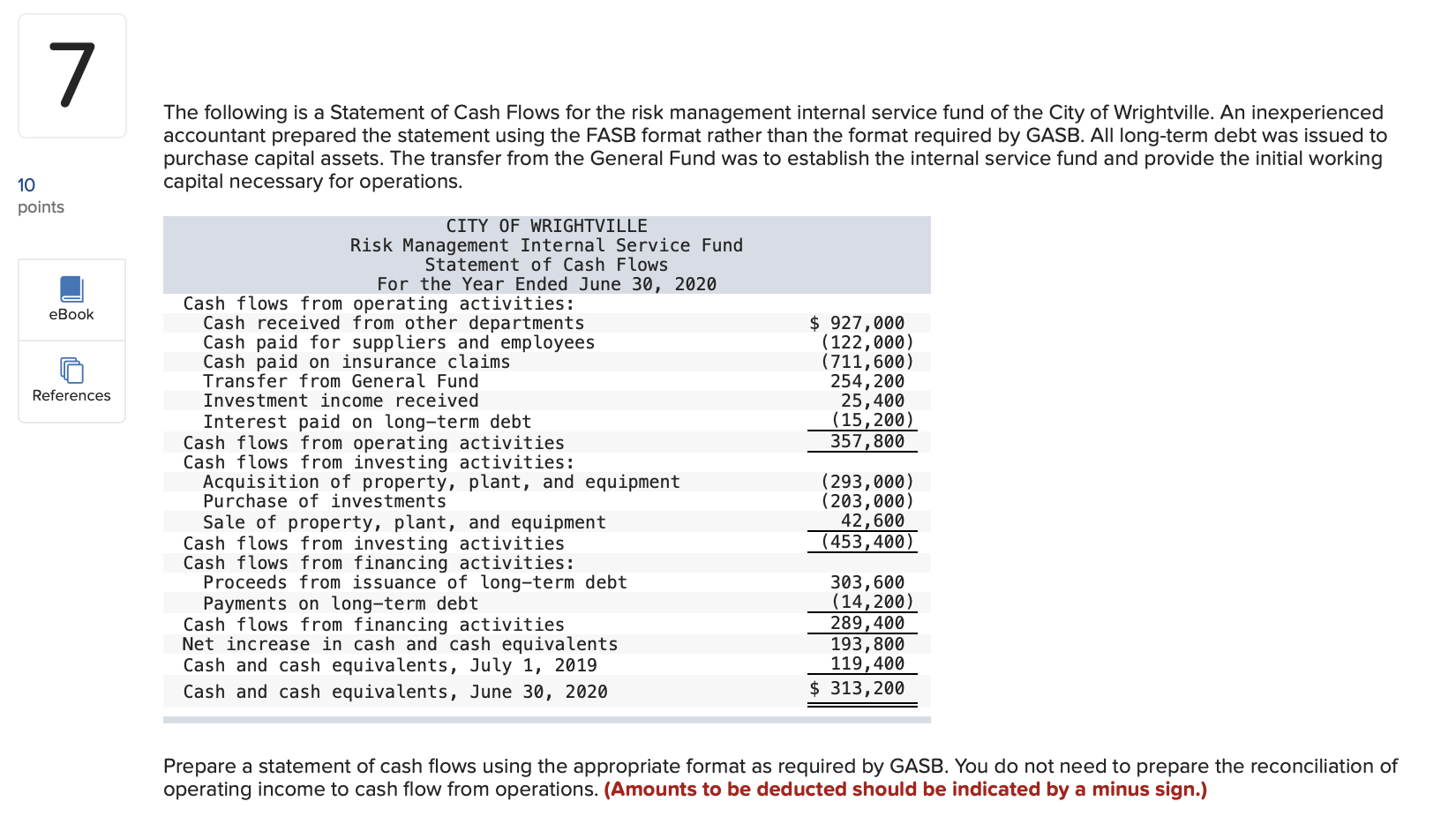

My partner and i are located in our 60s and seeking within ways to beat all of our expenditures whenever we retire. We sensed downsizing, but immediately following twenty seven ages our house and people still match all of us. Our home are ultimately taken care of that’s very in check except we love having the ability to pay for big fixes otherwise healthcare later. Create an opposing home loan seem sensible for people?

I am pleased you questioned this concern because so many men and women are within the just your role, trying to “decades set up” in lieu of proceed to a smaller sized, inexpensive family or a retirement people. But since you explain, keeping a huge house and you can buying health care and other prospective costs should be challenging.

Well done for the settling the home loan; which is a primary success and can yes assist your budget. For people who nevertheless find yourself lacking bucks, a property collateral mortgage (HELOC) otherwise a profit-aside financial is choice, but each other would want you to make monthly premiums. So when you recommend, a contrary financial could also seem sensible, offered you know what you’ll get to your as well as how they ties into your large monetary photo.

To your and additionally side, an other home loan can help you make use of a percentage of home’s equity without the need to make monthly installments. On disadvantage, the newest charges and appeal costs are typically more than those getting a money-aside refinance or HELOC. Whenever together with the amount of money your use, this can significantly rot the collateral that you’ve gathered inside your property. Why don’t we talk about more specifics so as that you’ll be able to build an educated choice.

Note: There are many categories of opposite home loan applications. I’m level (and you will advise you to merely believe) what exactly is called Home Equity Conversion Mortgages (HECMs) or “heck-ums.” This is because HECMs is regulated and you can insured from the national because of the Agencies out-of Casing and you will Urban Development (HUD) additionally the Government Property Power (FHA). Other kinds of contrary mortgage loans don’t possess this type of defenses.

Belle Fontaine bad credit payday loans no credit check open 24/7

Reverse mortgage principles

A contrary home loan is a loan that makes use of your residence since the equity. You are able to new proceeds getting anything from complementing your income, to paying down almost every other obligations, to creating a giant pick. Your house will remain in your identity as well as the earnings you found try taxation-totally free while the currency arises from that loan. On top of that, in spite of how far you borrowed with the an opposite mortgage, you simply cannot are obligated to pay more the value of your property (even if the financing balance try larger).

One of the biggest benefits associated with an other financial is the fact you’re not needed to build money if you remain of your property. Yet not, once you log off your house for more than 12 months, sell otherwise die, the newest outstanding loan must be paid also one notice-usually regarding the business of the home.

Qualification criteria

Not just anyone can get a contrary financial. Basic, the new youngest borrower have to be at the very least 62. As well as the household should be the majority of your home. You simply can’t take out an other financial toward one minute domestic or an investment property. You additionally can prove that you is also look after the property and spend assets taxation, insurance coverage, HOA charge, an such like.

Last but most certainly not least, you ought to individual your home downright (or those who have a mortgage must pay it well with sometimes the opposite mortgage proceeds or other money prior to they could use the proceeds for other things).

How much you could borrow

The total amount you might acquire is based on your (and your spouse’s) age, the value of your home, and you can interest levels. Brand new more mature you are, more collateral you’ve got, and also the lessen the interest rate environment, the bigger the amount you could potentially acquire.

There is a limit regarding how much you could potentially pull out brand new first 12 months and you may a complete limitation to exactly how much of the worth of your house you could borrow on. In the 2022, brand new HECM FHA mortgage restrict try $970,800. Very even if you reside worthy of $3 mil, new HECM is only going to allow you to borrow against $970,800 of their worthy of. You’ll then have the ability to use from thirty-five-75 % for the count, based on your actual age, interest levels, as well as how much guarantee you have got regarding the assets.

Unlocking various other retirement tips

Once you have the mortgage, you could potentially do the profit a lump sum, a specified amount to possess a fixed few years, monthly payments if you stay-in the house (tenure), an excellent standby personal line of credit to make use of when you want otherwise a mix of repaired or tenure money which have a type of borrowing.

There are a variety regarding methods for you to use an opposing home loan to your benefit. Particularly, you could use they to create a full time income “bridge” to allege large Societal Security professionals later, protect against being forced to promote property while in the a bear sector, pay for taxation into Roth conversion rates, purchase family home improvements, if you don’t pick a special home.

It is really not totally free currency

A face-to-face financial can carry will cost you all the way to several thousand dollars and you can normally total up to be much greater than a good conventional home loan otherwise HELOC.

As a general rule, loan providers have a tendency to fees: 1) mortgage insurance costs (initially and you may annual) 2) third-party fees step 3) origination percentage 4) notice and you will 5) maintenance fees. You can either shell out such costs initial otherwise by the financial support him or her throughout the years regarding the proceeds of one’s mortgage.

Money such costs commonly reduce the count you might borrow and consume aside in the a lot more of your house guarantee throughout the years-making quicker to the home. It’s important to understand that with a timeless financial your build security over time. Having an opposite mortgage, you fatigue equity which you have build through the years.

Certain summary

Reverse mortgages have gone as a result of many transform along the ages. Early they were tend to greatly sold as a way to expend on privileges otherwise employed by aggressive salespeople to get across-promote financially rewarding capital affairs. When you are this type of violations remain, nowadays there are way more defense.

Now, before you apply to possess good HECM, you might be required to talk with a therapist from a separate government-acknowledged property guidance agencies. You can check out HUD to track down a therapist, or name the department on step one-800-569-4287.

For the right anybody throughout the proper state, opposite mortgage loans are a distinctively efficient way to remain in your house during the senior years. However it is required to envision overall, weigh the advantages, will set you back and you will dangers.

What if certainly your enjoys a health problem? Exactly how have a tendency to a face-to-face financial perception a decide to ‘leave new family toward babies?” Or what if you merely pick that current household zero offered suits your needs? Chat away all these circumstances with your wife, your financial advisor, and perhaps actually the beneficiaries before you sign with the dotted line.